Market Timing Vs. Staying Invested: The Facts Head-to-Head

Addressing the giant elephant in the room, we are obviously with the staying invested camp. By focusing on our investment objectives and staying invested, it gives us an edge over the market timers who may be too distracted and affected by short-term news flow and headlines. But don’t take our word for it, the numbers do not lie. Here are a few facts to pique your interest:

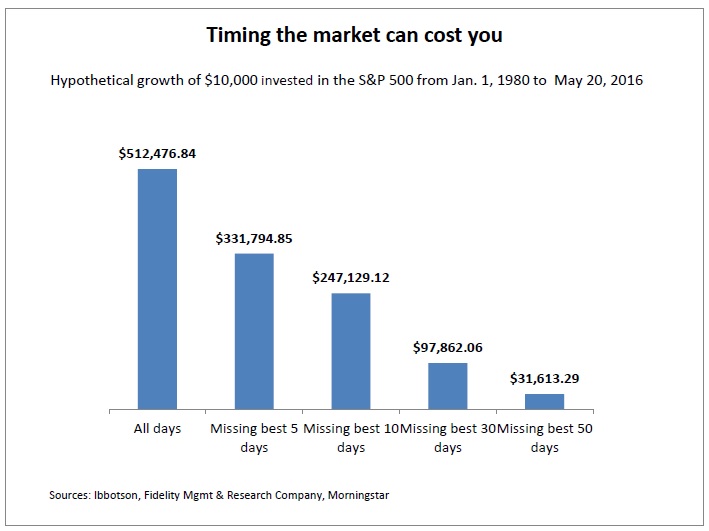

- Missing the best days can be costly

Market timers have a tendency to switch in to equity market when they see an opportunity to make a quick buck. Having accomplished their goal, they will immediately switch out. They will run this playbook over and over again whenever opportunity presents itself.

However, excessive movements in and out of the market can actually be counter-productive. As much as they are at risk of being caught out if the markets suddenly turn against them, they also risk missing out on the best days of a market rally.

Look no further than an analysis conducted in 2016 by Fidelity Investments and independent research firm, Morningstar. Just missing the five best days of the rally could mean the market timer’s returns are only $331,794.84 compared to the investor who remained invested; whose returns come up to $512,476.84. This meant a difference of $180,682 or 54% more of what the market timer could have achieved, had he not tried to time the market.

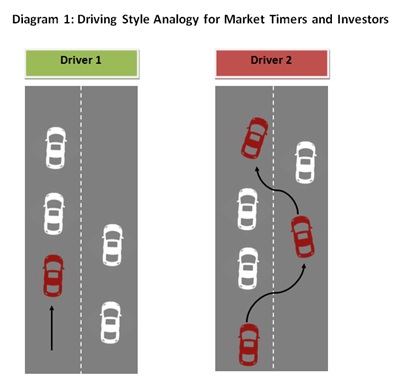

We think an analogy can be found to differentiate investors from market timers. Referring to Diagram 1, both drivers are heading to the same location with similar traffic conditions. Driving style though, differs considerably. Driver 1 patiently keeps in his lane while Driver 2 weaves in an out, in an effort to get to the destination faster.

Granted, Driver 2, may be able to get to his destination faster by a few minutes, but by moving out of lanes where he perceives to be slower and moving in to lanes where he thinks will give him a slight advantage, this increases his risk of being involved in an accident. This will come at the cost of his time and money, setting him back even further. Ultimately, will his actions be worth it? Can he truly beat the traffic?

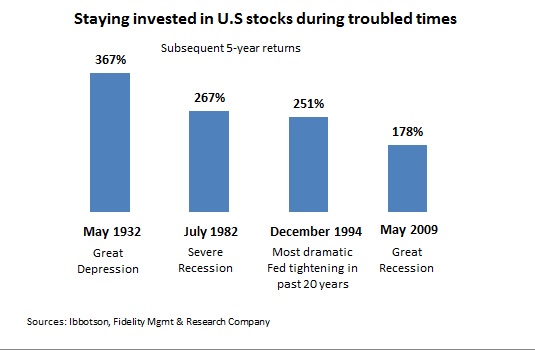

- Remain invested even through market volatility to generate superior returns

Fear is an inherent human emotion, so it’s quite natural to assume that investors fear to hold on to their investments especially during what seems to be, market-moving events.

However, wise investment decisions are usually made without emotional interference. Besides that, the intensity and fervour of these market-moving events and other headline grabbing news usually die down after a couple of weeks.

Riding through short-term market swings isn’t such an unacceptable proposition that some make it out to be. On the contrary, it can pay off to remain invested rather than switch out at the first sign of trouble. A 2015 study by Fidelity Investments vindicates our case:

- Lessons to be learnt from successful investors

In order to achieve superior returns, successful investors have stayed invested throughout the market cycles, rode out short term volatilities and even looked to add more when market crashes presented them with bargains. Here are 4 famous investing gurus:

| Investing Guru | Average annualized returns per year during period assessed | Quote |

|---|---|---|

| Peter Lynch | 29.2% a year from 1977 to 1990 [1] (Fidelity Magellan Fund) |

Invest in a business you understand. |

| Warren Buffett | 20.8% a year from 1965 to 2017 [2] (Berkshire Hathaway) |

I never attempt to make money on the stock market. I buy on assumption they could close the market the next day and not re-open it for five years. |

| Benjamin Graham | 20% a year from 1936 to 1956 [3] | In the short run, the market is a voting machine but in the long run, it is a weighing machine. |

| John Templeton | 15% a year from 1954 to 1992 [4] (Templeton Growth Fund) |

The stock market is not a casino, but if you move in and out of stocks every time they move a point or two, or if you continually sell short… or deal only in options, or trade in futures, the market will be your casino. And, like most gamblers, you may lose eventually — or frequently. |

Sourced from:

Conclusion

You have to accept that you can never be the first or the fastest to react to the whims of the markets and the shifts in sentiment. Markets are notoriously hard to predict over the shorter term. A better way is to think ahead of the crowd; 2 or 3 years down the road. Pick a good stock or a better-managed Unit Trust Fund and hang on through the short term market trends. Let time do the heavy lifting for you. Superior returns can be generated by riding through market volatility and staying invested.

Meanwhile, the search for the best entry point may turn out to be futile. If investing in 1 lump sum into the equity market is something that concerns you, try investing systematically whether through Value Averaging or Cost Averaging. A disciplined investing strategy removes emotional biases from your decision making.

All of us are investing for a reason, be it for our eventual retirement or children’s education. The time until the life goal spans many years. To put things in perspective, if you are a 40 year old adult and saving up for your children’s education in university which is 10 years’ away, day-to-day fluctuations in the equity market should not bother you at all. Invest for the long term and look at the bigger picture. If you keep thinking of the trees, you will end missing the forest.

Remember, it is time in the market, not timing the market.